Retailer-Owned Agents May Become the Next Retail Media Gatekeeper

The next retail-media gatekeeper may not be a search-results page. It may be the retailer-owned agent that interprets a shopper’s intent, chooses the shortlist, completes the basket, and measures what happened next.

Retail media was built around a simple proposition: a retailer owns the digital shelf, brands pay to be more visible on it, and the retailer can connect exposure to a sale. That model produced a large and durable business because the shelf was easy to see. Search results, category pages, product cards, and sponsored placements gave everyone a shared mental model of where influence lived.

A retailer-owned shopping agent changes the location of that influence. A shopper does not have to scan a page of products and decide what to click. They can ask for a recommendation, add constraints, explain a use case, and receive a shortlist—or a basket—inside a conversation. If the retailer owns that conversation, it can potentially own a more valuable point in the decision process than the old search-results page ever did.

That does not mean every retailer assistant will become an advertising gatekeeper. It does mean the ingredients are beginning to converge: proprietary shopping data, live catalog and fulfillment information, a recommendation interface, retail-media relationships, and closed-loop measurement. The company that operates all five has a plausible claim on the next commercial decision moment.

Core argument

A retailer-owned agent becomes a retail-media gatekeeper when it does more than answer questions. It must interpret intent, control the recommendation shortlist, connect that choice to retailer data and checkout, and offer brands a measurable way to participate without making the advice untrustworthy.

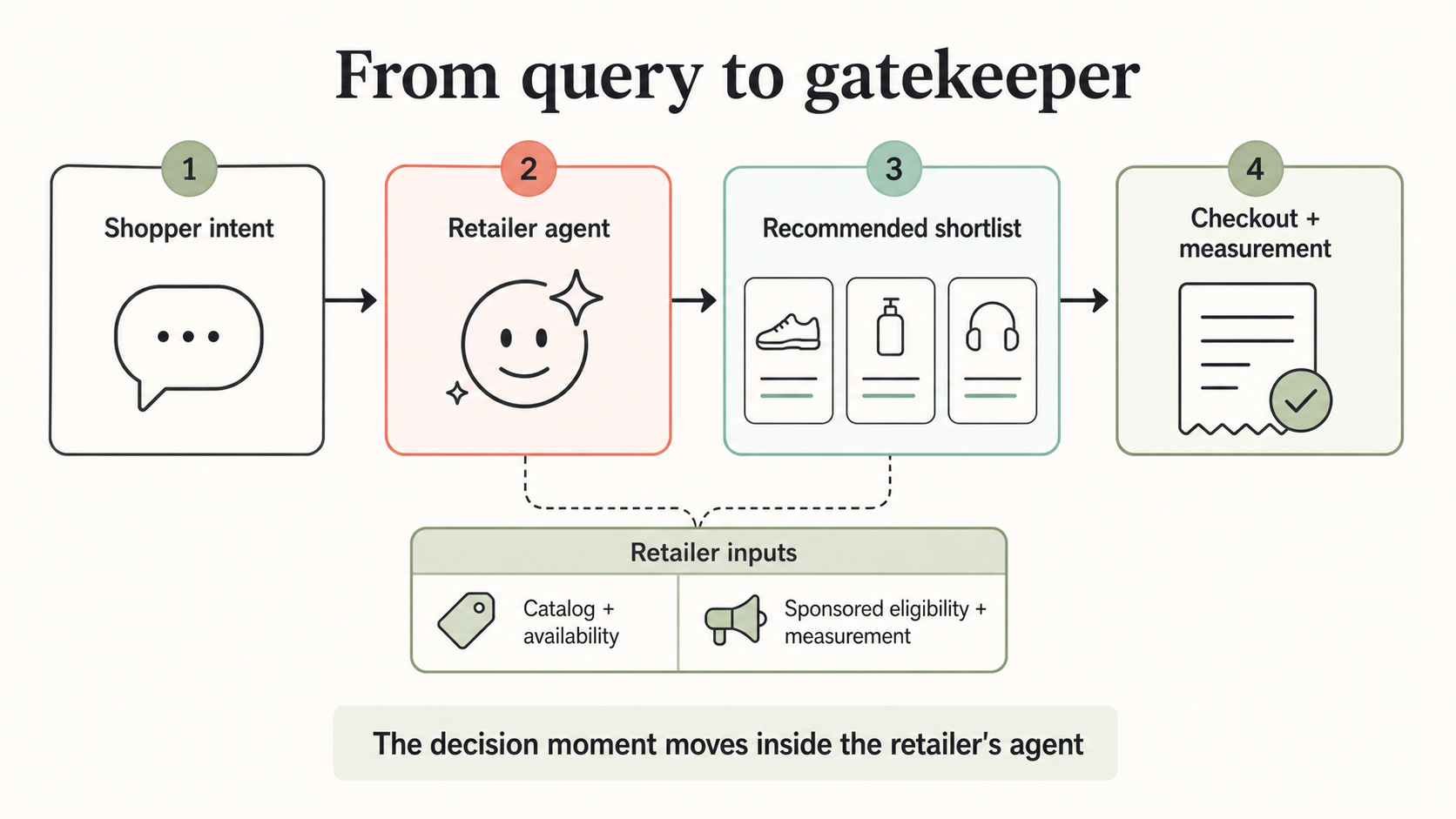

The gatekeeper model

The diagram is deliberately simple, but the strategic change is not. In conventional retail media, a brand competes for a position after the shopper has expressed a keyword. In an agent interaction, the retailer can first ask what the shopper means. “A quiet blender for a small kitchen” contains budget, usage, space, noise, brand preference, availability, and delivery constraints. The conversation creates a richer decision context before a product is ever shown.

That is the first gate. The second is the shortlist. A retailer agent may decide which products are eligible to be considered, how alternatives are compared, which policies or reviews matter, and whether a sponsored option belongs in a clearly separated module. The third is the transaction: retailers can see inventory, delivery promises, substitutions, memberships, returns, and the final order. Together, those steps offer a tighter loop between a brand’s commercial participation and a measurable result.

Walmart shows why this is no longer a theoretical model

Walmart’s Sparky is an early but instructive example. The company introduced the assistant as a shopping experience that can synthesize reviews, make recommendations for occasions, support product comparisons, and eventually help with tasks such as reordering essentials and planning purchases. Walmart has also said it is preparing advertising strategies and agent-specific discovery paths for a world in which agents shop differently from humans.

The commercial evidence is still early, and should be treated that way. At a 2026 investor event, Walmart’s CFO said roughly half of app users were engaging with Sparky in some way, and that customers who bought through the Sparky experience had baskets 35% higher than otherwise. Those are company-reported figures, not an independent causal study. But they show why a retailer may care about owning the agent surface: the assistant is not merely a service feature if it can improve conversion, basket-building, and the usefulness of first-party data at the same time.

Walmart Connect has already said it tested advertising formats tied to Sparky in 2025 and would continue developing them in 2026. Meanwhile, Walmart reported global advertising growth of 37% and U.S. Walmart Connect growth of 44% excluding VIZIO in its May 2026 results. The relevant conclusion is not that Sparky already runs a mature sponsored-ranking auction. It is that a large retail-media business has a direct incentive to find commercial formats that fit its own conversational shopping environment.

The agent changes what “placement” means

Retail media historically sold visibility in a known container: the sponsored slot, the search rank, the display unit, the off-site audience. An agent has a different container. It can recommend three options, explain why one fits, ask a follow-up question, create a bundle, or put an item in the cart. It can do all of this without showing the shopper a conventional category page.

That makes placement both more valuable and more dangerous. More valuable because it can be attached to a highly specific, declared need. More dangerous because the agent’s language feels like advice. A paid listing can coexist with a page of organic search results; a paid recommendation inside a personal conversation needs a much clearer boundary.

Amazon’s current advertising approach illustrates the direction of travel. Amazon Ads says sponsored ads can surface products and brands within Alexa for Shopping conversations, and that Sponsored Products and Sponsored Brands prompts can open product-related conversations. Target, for its part, has described a ChatGPT pilot in which sponsored, contextual, clearly labeled ads from Target and Roundel partners appear separately from the answer. These are not interchangeable implementations, but they share a premise: commerce media is testing how to follow the shopper into conversational decision-making.

The real product is not the answer. It is the governed shortlist.

The most important new asset may be neither a chatbot nor an ad unit. It is a governed recommendation pool: the set of products an agent is allowed to consider, enriched with accurate catalog data, availability, delivery promises, product facts, reviews, brand policies, commercial eligibility, and rules about disclosure.

For retailers, that pool can be a defensible asset. It is informed by data that general-purpose assistants may not have in real time: local stock, substitution logic, delivery windows, membership benefits, product returns, and actual purchase behavior. For brands, it introduces a new question: what must be true for a product to be eligible, not simply visible?

| Old retail-media question | Agent-era question | Brand implication |

|---|---|---|

| How do we win a sponsored slot? | Are we eligible for the agent’s shortlist? | Clean product, offer, availability, and policy data become a prerequisite. |

| What keyword should we bid on? | Which intent patterns should we serve? | Brand teams need use-case, constraint, and comparison language—not only keyword lists. |

| Did the shopper click? | Did the agent recommend, explain, add, and convert? | Measurement must expand beyond impressions and clicks. |

| Was the ad labeled? | Was commercial influence distinct from advice? | Disclosure and auditability become part of brand safety. |

Why retailers have an advantage—and why they may not keep it

A retailer-owned agent has a natural advantage at the moment of fulfillment. It knows whether a product can arrive today, whether a basket qualifies for membership benefits, what inventory is nearby, and what the customer has previously bought from that retailer. It can connect discovery to checkout without handing the shopper to another site. That is a powerful basis for relevance and measurement.

But retailer ownership is not the same as permanent control. Google’s Universal Commerce Protocol work and Universal Cart vision point to another future: independent or general-purpose interfaces can carry a shopping task across multiple merchants while retailers remain merchant of record. In that world, the retailer-owned agent is one important gatekeeper among several—not the gatekeeper.

That competitive tension is healthy. It means retailers will have to earn the consumer’s preference by being useful, transparent, and reliable, rather than relying only on closed inventory. It also means brands should resist building a strategy that assumes a single agent surface will control all discovery.

What brands should ask before the format hardens

What makes a product eligible for recommendation? Ask for the data, quality, fulfillment, and policy conditions that determine inclusion. “Optimize for the agent” is not a useful answer unless the criteria are concrete.

Where does paid influence begin and end? Sponsored modules can be legitimate if they are explicit. Brands should want to know whether payment affects eligibility, ordering, generated language, or only separately labeled placements.

What is measured, and who can audit it? Closed-loop measurement is valuable, but it cannot be a black box. Seek reporting on recommendation exposure, shortlist inclusion, add-to-cart behavior, conversion, returns, and incrementality where possible.

What customer relationship survives? Participation in a retailer agent can create discovery value, but brands should understand what customer, query, and performance data return to them—and what remains inside the retailer.

How portable is the readiness work? Better product facts, availability, policies, and use-case content should improve eligibility across many agent surfaces, not lock a brand into one retailer’s rules.

The trust constraint is not optional

The best retailer agents will have to separate two things that existing retail media sometimes blurs: relevance and commercial influence. A shopper can accept a clearly labeled sponsored option, especially when it is distinct from the assistant’s answer. What they are less likely to accept is an agent that presents a paid result as disinterested advice.

That is not only a consumer-experience issue. It is an economic one. If the assistant loses trust, shoppers stop sharing the preferences and constraints that make agentic recommendations valuable in the first place. The same data flywheel that makes a retailer agent powerful depends on the user believing the agent is helping, not merely selling.

The bottom line

Retailer-owned agents may become the next retail-media gatekeepers because they can move the decision moment from the visible shelf into a conversational flow they operate. They can interpret intent, assemble a shortlist from live retail data, connect it to checkout, and measure the outcome. That is a more intimate form of influence than a sponsored search slot.

But “may” matters. The model will only endure if commercial participation is transparent, recommendation rules are governable, and shoppers retain real choice. Brands should prepare for agent eligibility and agent-era measurement now—while insisting that the new gatekeeper does not turn useful advice into invisible advertising.

Frequently Asked Questions

What makes a retailer-owned agent a retail-media gatekeeper?

It becomes a gatekeeper when it controls the path from shopper intent to a recommendation shortlist and checkout, while the retailer can connect brand participation to closed-loop measurement. A chatbot without those decision and measurement layers is not yet a retail-media gatekeeper.

Does this mean retailer agents will replace retail-media search ads?

Not immediately. Conventional search and display surfaces remain valuable. The likely near-term shift is that retailers test conversational placements and agent eligibility alongside existing formats, then learn which commercial models preserve shopper trust.

Will paid brands determine an agent’s recommendations?

There is no basis to assume that. Some retailers are testing sponsored and contextual formats, but brands should demand clear disclosure of whether payment affects inclusion, ranking, generated language, or only separately labeled placements.

What should a DTC brand do first?

Make product, inventory, shipping, returns, and use-case data complete and current. Then ask retail partners for explicit criteria governing recommendation eligibility, sponsorship, reporting, and customer-data access.

References & Further Reading

[1] Walmart: The Future of Shopping Is Agentic. Meet Sparky.

[2] Walmart: Inside Walmart’s strategy for building an agentic future

[3] Walmart Connect: The next generation of AI-powered retail media

[5] Walmart JPMorgan Retail Roundup 2026 transcript

[6] Amazon Ads: What agentic shopping means for advertising

[7] Target and Roundel test advertising in ChatGPT

[8] Google: Agentic commerce tools and protocol for retailers and platforms

Continue Exploring

AI Shopping Could Break Retail Media Before It Rebuilds It

Why the old visible shelf-space model may not transfer cleanly to conversational recommendations.

Amazon Is Building a Moat Around Agentic Shopping

A research briefing on platform control points across discovery, merchant participation, checkout, and access.

How Retailers Stay Visible When AI Shopping Agents Choose the Products

A practical guide to improving agent-readiness through product data and trust signals.